A Glimpse At Personal Finance in Australia, The United States and The United Kingdom

This report examines financial behavior across Australia, the United States, and the United Kingdom, highlighting spending, saving, retirement planning and investment patterns in these particular nations.

In addition, this report evaluates basic financial literacy by asking respondents about their understanding of key concepts to reveal the correlation between knowledge and practice. By examining these insights, we are better able to understand global financial habits and the confidence gaps that influence them.

Financial literacy refers to how well an individual understands financial skills, and it is a foundation for managing personal finances and understanding economic conditions. It includes how people budget and invest their money, understand taxes and economic circumstances, and how well they grasp financial principles.

Financial literacy in Australia

Despite the fact that more than half of Australians (55%) do not feel confident in their financial understanding, Australia is the leading nation in financial literacy scores, showcasing how strong Australia is in terms of individual money management and understanding.

Our survey results show that although less than half of Australians surveyed (45%) described themselves as confident in their understanding of financial principles, 4 out of 5 can correctly define compound interest (82%) and also understand how inflation impacts purchasing power (86%). Australians seem to know more about money management than they realise!

Financial literacy in the United States

Although there is a gap between confidence and knowledge levels in Australia, it is more severe in the United States. Americans are the least secure of the populations we surveyed in terms of confidence, as only one third of Americans (36%) describe themselves as confident in their financial literacy.

Despite this relative lack of confidence, the majority of Americans excel in understanding mortgages (87%), and 4 out of 5 understand inflation and compound interest. The discrepancy between comprehension and confidence could be creating an issue in application.

Financial literacy in the United Kingdom

Similarly to Australia and the US, there is a discrepancy in how people in the UK describe their financial literacy compared to reality. People in the United Kingdom were mostly able to correctly define key financial terms like compound interest and inflation despite 2 in 3 (63%) describing themselves as “not confident” or “somewhat confident” in their financial understanding.

This lack of confidence may be partially due to the ways in which people in the UK access information and guidance about personal finance. Whereas Australians look to blogs and online guidance, people in the UK tend to prefer books as a source of information and around a third (37%) of people in the UK have spoken to financial advisors. This inaccessibility of information may be a root cause for limited confidence in financial literacy.

If financial literacy tells us about how knowledgeable populations are about financial principles, then spending habits tell us about how that knowledge translates into actions. Between the nations we surveyed about their financial habits, there were major differences in how people spend their money.

Spending habits in Australia

More so than in the UK and US, Australians have shown a significant move towards more modern ways of spending, with debit cards and mobile payment apps dominating how Australians prefer to pay. In fact, one-fifth (21%) of Australians have adopted mobile payment apps as a key way of spending money, showing a broad cultural shift towards digital payment options.

When it comes to spending on non-essentials and special occasions, Australians are both more organized and more lavish with spending. 40% of Australians budget 10-20% of their income for discretionary spending. With the average salary in Australia being $85,000 per year, this accounts for an average of $8,500-$17,000 per year on non-essentials, and is more than the other countries we surveyed.

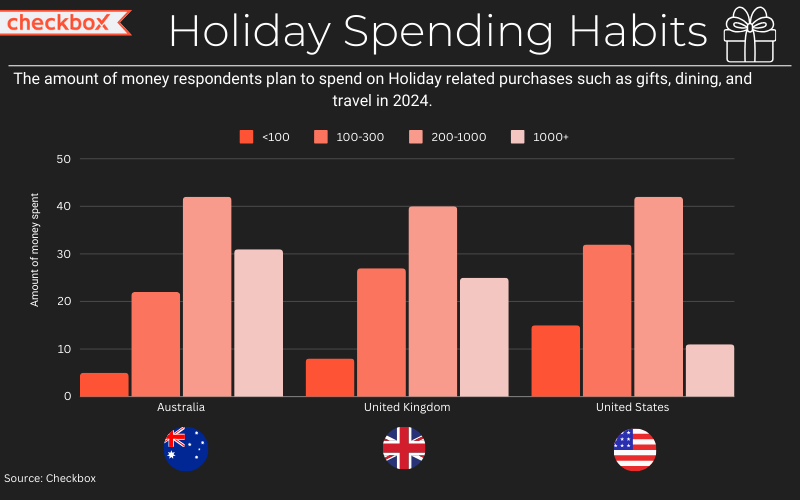

As well as budgeting highly for non-essentials, almost a third of Australians splash out more than 1,000 AUD on their holiday budgets – the highest holiday spend of the three nations.

Spending habits in the United States

Despite being famous for loving the holiday season, Americans tend to be a little more reserved when it comes to festive spending. Compared to a third of Australians, only 11% of Americans budget more than $1000 for holiday spending, and a third (32%) only budget $100-300.

However, a third of Americans (31%) do not budget at all for their holiday spending. Around a quarter of Americans (24%) noted that they struggle with impulse spending, while a third (36%) rely on credit cards for everyday spending. Between a lack of holiday budgeting, a reliance on credit, and a tendency towards unplanned expenses, many Americans appear to struggle with budgeting.

At the checkout, debit cards remain the most popular payment method with almost half of Americans (45%) spending with a debit card. For everyday purchases, around a third of Americans (36%) still choose credit cards. With more Americans choosing to pay with debit and credit cards compared to only 12% choosing to pay with mobile payment apps, it seems that Americans prefer more traditional ways to pay.

Spending habits in the United Kingdom

In the UK, spending habits showed polarization. While 27% of people in the UK set and stick to their holiday budgets, more than a third (37%) spend with no budget at all. This suggests that the extremes of over-spending and tight budgeting both exist in the UK.

When it comes to paying, people in the UK vastly prefer to use debit cards than any other payment method, with almost 60% sticking to the more traditional card payment option, which does not rely on credit or debt spending. Again showing a traditional attitude towards payment behaviors, cash usage is preferred by 6% of people in the UK compared to only 4% in Australia.

Saving habits in Australia

Australians are good savers. In fact, of the three nations surveyed, Australia is the population with the highest proportion of savings accounts. 96% of Australians have savings accounts, with a quarter of Australians(25%) saving more than 20% of their income, highlighting that in Australia there is not only an intention, but also a regular action, towards saving for the future.

This culture of saving has created a higher level of confidence in their ability to save than in the US and UK. However, this confidence has limitations, with just over a quarter of Australians noting impulse spending (27%) and debt payments (25%) as a blocker to their ability to save.

Saving habits in the United States

Americans save the least out of the nations surveyed. Our research found that 40% of Americans save less than 5% of their income, which when considering the national salary of $62,000, could be as little as $260 a month. When asked why, more than three quarters of Americans cited a high cost of living (77%). Data from Forbes shows that in 2022, inflation in the USA hit its highest level since the 1980s, which has had an impact on how much Americans are able to save.

For most, there are good intentions – 10% plan to open savings accounts, with the leading goal being building up an emergency fund. Our research also found that a quarter (25%) of Americans turn to credit cards instead of savings when they need immediate financial assistance. To build up a stronger culture of savings, 17% of Americans feel they would be able to save more effectively if they had better financial knowledge.

Saving habits in the United Kingdom

Saving habits in the United Kingdom are somewhere in between those of Australians and Americans, with 91% of people in the UK having savings accounts but with challenges like the high cost of living and debt payments representing practical impediments to saving more.

There is a culture of saving for the future in the United Kingdom. Whereas in other nations, many individuals are saving for personal goals, in the UK the main motivators to saving are buying a home (37%) and retirement funds (31%). Just 1 in 10 savers stated that they had no specific purpose for their savings.

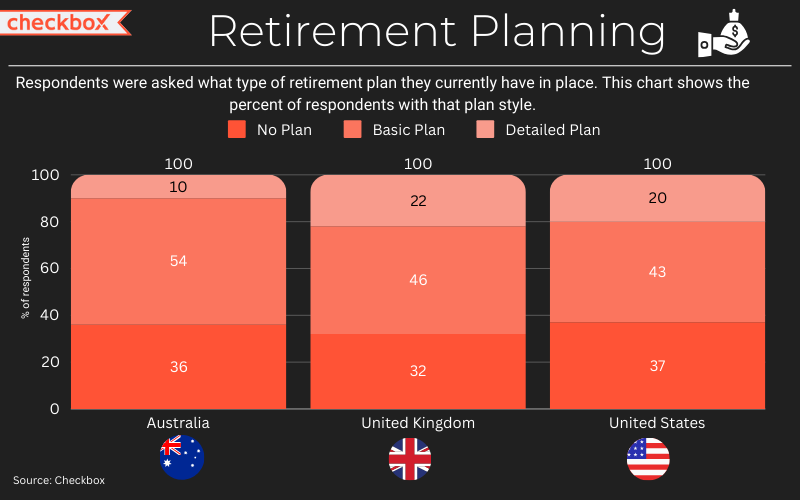

In the UK, we saw that saving towards retirement and later life is a key motivator in saving money. How individuals consider their long-term financial needs is an interesting indicator of financial culture. Our survey highlighted that there are wide discrepancies between nations, with people in the UK planning more specifically, Australians being well covered by basic retirement plans, and America falling behind with many feeling insecure about their retirement financial plans.

Retirement planning in Australia

When it comes to preparing for retirement, Australians have a good grasp on basic retirement packages but do not tend to have detailed plans. While 40% of Australians surveyed started saving for their retirement before the age of 25, 19% of Australians do not think themselves knowledgeable about retirement options.

This indicates that Australians know that they should save towards retirement, but do not have a good sense of the right ways to save or what their different options may be. This is further supported by almost three-quarters (71%) of Australians saying they do not feel confident that they are saving enough for retirement.

The combination of a large proportion of Australians beginning to save for retirement early but the majority feeling that their savings are insufficient could speak to the impacts of rising retirement costs and recent inflation on savings in Australia.

Retirement planning in the United States

The United States lags behind in retirement planning, with over a third of Americans (37%) having no retirement plan whatsoever. Of those who are planning ahead for retirement, only a quarter begin doing so before the age of 25, while almost 60% of Americans feel insecure in their retirement plans.

Part of this issue in America is an individual knowledge gap. Almost half (42%) who do save towards retirement do so through a basic 401k scheme, while a quarter (24%) feel they lack knowledge on their retirement savings options. The knowledge gap could be due to the safety net of employer-sponsored schemes like the 401k. With many opting for the provided option, few are investigating retirement options further.

Retirement planning in the United Kingdom

The UK has a strong retirement planning culture, with 22% of people in the UK having detailed retirement plans. Retirement planning is one of the key motivators for saving money.

Despite a high proportion of people in the UK saving in a detailed way for their retirement, there are still gaps in knowledge that need to be addressed. People aged 45-54 have the lowest confidence levels of all in the UK, feeling insecure in their retirement savings. Despite this, the UK has the highest levels of awareness of pension systems and their options, which likely contributes to the overall strength of planning.

Investment is often seen as one of the most complex aspects of financial literacy, with many opting instead for simpler ways of saving. Across all of the nations we’ve surveyed, there are clear indications that individuals do not fully understand investment options and lack confidence with them. This lack of understanding is an area of interest and growth for organizations within the financial services industry, which can offer educational resources to help expand the popular understanding of investing.

Investment patterns in Australia

Australians appear to be quite wary of investing, with most instead prioritizing saving through traditional savings accounts.

Two thirds (66%) of Australians use online resources to educate themselves on investment and to access financial advice. This highlights that a growing number of Australians are interested in learning more about investment through the sources they have most access to.

Investment patterns in the United States

The US has an interesting relationship with investing. While Americans tend to be familiar with more entry-level investments like a 401k, only 12% report being very knowledgeable about their investment options. This speaks to a reliance on basic level plans typically provided by employers, with the majority of Americans not feeling confident to invest independently.

As in Australia, it is clear that individuals are aware of their lack of financial knowledge, and show a desire to learn more about these topics. Almost half (46%) of Americans rely on self-research to get a better understanding of investment. This includes books, social media, and popular podcasts such as the Goldman Sachs Exchanges show, The Personal Finance Podcast, and The Ramsey Show. This indicates that access to resources may have been a blocker to financial literacy pertaining to investment in the past, but many are working to change this.

Investment patterns in the United Kingdom

In the UK, there is a mixed level of confidence in investment. While 40% describe themselves as being somewhat knowledgeable about investment options, almost half of people in the UK (48%) answered questions about bond prices and interest rates incorrectly. This perhaps implies that people in the UK think they know more about investing in theory than they do in practice.

This plays out in the ways that people invest in the UK, with a cultural reliance on pension schemes being prevalent and a very limited level of diversity in investment patterns. In the UK, then, we can see that though most have reasonable confidence in their understanding of investing, few are able to showcase this knowledge through diverse investment portfolios.

Conclusion

Financial literacy and behaviours vary significantly between Australia, the US, and the UK, yet common themes emerge. There is a shared desire among respondents to better navigate their finances and secure their futures, but this survey revealed that respondents are not confident in their knowledge, and indeed, did not correctly answer many of the financial questions.

Contact us

Fill out this form and our team will respond to connect.

If you are a current Checkbox customer in need of support, please email us at support@checkbox.com for assistance.